April 27, 2020

February 3, 2018

Measuring racial segregation, homeownership rates, home values since 1940

Drawn in cities across the country to separate "hazardous" and "declining" from "desirable" and "best," codified patterns of racial segregation and disparities in access to credit. Now economists at the Federal Reserve Bank of Chicago, analyzing data from recently digitized copies of those maps, show that the consequences lasted for decades.

As recently as 2010, they find, differences in the level of racial segregation, homeownership rates, home values and credit scores were still apparent where these boundaries were drawn.

Continue reading "Measuring racial segregation, homeownership rates, home values since 1940" »

January 24, 2018

STEPS I TAKE TO COUNTERACT GENTRIFICATION WHILE LIVING IN A LUXURY BUILDING IN BROOKLYN

Complain about the doorman service to my management company;

but also be super nice to the doormen because my luxury building is giving jobs to the local community;

but also make sure to leave a bad review on the management company's website so people avoid renting an apartment in my luxury building,

which in turn might make my luxury building's rent prices go down

and thus making it more accessible to the local community to get a place there at an affordable rate

and then getting the snobby tenants to complain about the new tenants using the common washer/dryer for their entire family

and how they have very loud music,

eventually getting so annoyed they will not renew their lease

and force them to seek out a fancier luxury building in which to live,

resulting in even lower rents in my luxury building,

rendering my luxury building a luxury building for the people.

August 16, 2017

GSEs took better care of foreclosed homes in working- and middle-class white areas than of equivalent homes in black and Latino communities ?

The mortgage crisis that ravaged the economy eight years ago was especially damaging to African-American communities, where homeowners who qualified for affordable mortgages were often steered into high-priced loans that paid rich returns to mortgage brokers and lenders while leaving borrowers vulnerable to default.

The ensuing glut of vacant homes drove down property values almost everywhere. But minority communities suffered disproportionately, widening the already considerable wealth gap between white and minority households.

One big reason for these disparities, according to a federal lawsuit filed by a coalition of fair housing groups, was that companies like the mortgage giant Fannie Mae took better care of foreclosed homes in working- and middle-class white areas than of equivalent homes in black and Latino communities. The plaintiffs, led by the National Fair Housing Alliance, say they reported this problem as early as 2009 and that they filed suit against Fannie Mae only after it continued to neglect foreclosed properties it owned in African-American and Latino neighborhoods.

July 31, 2017

McMansion is logical progression

Housing has always been governed by a simple rule: As people become richer, they spend more money on their homes.... Spending more money has usually meant making the home bigger.

This happened in Renaissance Italy, 17th-century Holland, and 19th-century England. It also happened in the prosperous second half of the 20th century in the United States.

Some statistics: In 1950 the median size of a new house was 800 square feet; by 1970 this had increased to 1,300; 20 years later it had grown to 1,900; and in 2003 it stood at 2,100. More than one-third of new houses built today exceed 2,400 square feet.

-- reason

July 26, 2017

McMansion / Harvard Joint

People who are shopping for homes in a certain neighborhood expect certain amenities in those homes, says Kermit Baker, director of the remodeling futures program at Harvard University's Joint Center for Housing Studies.

"If you're not keeping up with other homes in the neighborhood, you may have home buyers walk away from it. There's a limited number of folks who want to buy assuming they're going to have to do a significant remodeling project".

-- 2007

July 25, 2017

I bought a house in humilty

I bought a house about two years ago. I got preapproved for a fixed rate loan and then found the home. My lender was absolutly amazed that I bought a home for significantly less than the amount for which I qualified. Said he's never seen that and that, in fact, people often come back needing the loan amount increased. McMansions are going up all around my pre-war bunglaow. I think Americans are crazy.

Hecate. (dead link http://www.haloscan.com/comments.php?user=atrios&comment=111253857282298328#2605269 ) Modern Pict | 04.03.2005

July 20, 2017

FHFA's rules: "very low-, low-, and moderate-income" defined

The FHFA's rule defines the terms "very low-, low-, and moderate-income":

The term ''low-income'' means--(A) in the case of owner-occupied units, income not in excess of 80 percent of area median income; and(B) in the case of rental units, income not in excess of 80 percent of area median income, with adjustments for smaller and larger families

The term ''moderate-income'' means-- (A) in the case of owner-occupied units, income not in excess of area median income; and (B) in the case of rental units, income not in excess of area median income, with adjustments for smaller and larger families

The term ''very low-income'' means-- (i) in the case of owner-occupied units, families having incomes not greater than 50 percent of the area median income; and (ii) in the case of rental units, families having incomes not greater than 50 percent of the area median income

July 3, 2017

McMansions became the ultimate symbol of living beyond one's means. Unlike your standard mansion, McMansions aren't just large -- they are tackily so. Looming over too-small lots, these cookie-cutter houses are often decked out with ersatz details, like ch

McMansions became the ultimate symbol of living beyond one's means. Unlike your standard mansion, McMansions aren't just large -- they are tackily so. Looming over too-small lots, these cookie-cutter houses are often decked out with ersatz details, like chandeliers and foam-filled columns. While their features mean they can command a decent price, many of these houses are shoddily built.

Since a "McMansion" is in the eye of the beholder, Zillow doesn't have a targeted way of tracking them nationwide. For this article and the video above, they approximated the category by focusing on houses built after 1980 that were greater than 3,000 square feet but less than 5,000 square feet. They also looked for houses located on streets where the homes are similarly sized, on similarly sized lots, and built within six years of each other, to isolate cookie-cutter communities.

A culture of house flipping helped to quantify certain home improvements, like the addition of colossal marble islands and palatial foyers designed to grab the attention of buyers. That gave these houses even more of a cookie-cutter feel.

Architecture critic Kate Wagner has dedicated her website, McMansion Hell, to explaining why these houses rub people the wrong way.

June 23, 2017

McMansions no more (Leigh County, PA)

Bethlehem Township developer Abraham Atiyeh announced two weeks ago that he's building a downtown Bethlehem development of town homes starting at $129,000, and national builder Pulte Homes has halted its large-home building in the area and last winter began marketing a new home, called "The Lehigh", with 1,050 square feet and starting price of $139,000.

McMansions No More ** Fewer behemoth homes may be built in the Lehigh Valley as turmoil in the housing market opens the door for smaller, more affordable living

Morning Call - Allentown, Pa.

Author: Matt Assad

Date: May 25, 2008

Start Page: A.1

Section: National

Text Word Count: 2299

[Via McAll]

More: McMansions.

January 31, 2017

New York City Has Been Zoned to Segregate

New York City Has Been Zoned to Segregate

A new book argues that poor communities of color are hurt by the city's zoning and housing policies.

Today, historical color lines are being redrawn through a concentration of wealth and the displacement of communities of color. In New York, that phenomenon may be spurred in part by the city's well-intentioned land-use policies. Various types of rezoning--upzoning and mixed-use zoning, for example--have inadvertently but disproportionately harmed poor neighborhoods. That's the central argument of Zoned Out!, a new book edited by Tom Angotti, an urban planning professor at the City University of New York, and housing advocate Sylvia Morse.

we talk about in the book is the watering down of the word "affordable." Affordable housing used to imply that it was housing for people who had less money, who needed help affording housing. Now, it basically means anything that meets the federal guidelines for rent not costing more than 30 percent of household income, and really there's a lot of room to obscure which groups you're serving through affordable housing. I think that's a very New York City-specific context. Of course, we still have the old school, low-density NIMBYism, which we talk about [in the book].

Continue reading "New York City Has Been Zoned to Segregate" »

May 15, 2016

Great Peconic Bay

"Brooklynites get the North Fork, period."

-- Sheri Winter Clarry, an associate broker with the Corcoran Group Real Estate on the North Fork in Southold, also attributed the uptick in buyers from Brooklyn to the region's "laid back, chilled vibe" and its growing status as a family-friendly second-home haven for foodies and oenophiles.

The magnets that draw city dwellers include the area's burgeoning farm-to-table movement, new craft breweries and distilleries, wineries, farm stands, antiques shops and seasonal agri-tainment activities like apple-, berry- and pumpkin-picking. Niche farms offer locally raised meat, goat cheese, organic greens and hops for making beer.

"Farms have upped their game like crazy, vineyards have upped their game, restaurants have upped their game," Ms. Clarry said. "It's really translated into the North Fork coming into its own. The food industry has helped people not just day-trip, but fall in love with it and move out here."

March 25, 2016

Suburban Jungle

"Neither of us really wanted to live in the suburbs," he said. They came across Suburban Jungle while attending a baby industry event last May and spent an hour and a half on the phone with a consultant who sent them town reports on Harrison and Rye in Westchester County and Darien and Greenwich in Fairfield County.

"They could tell us more than a broker is legally allowed to tell us," Mr. Allen said. "Because they were moms living there with their kids," he added, the strategists not only knew which areas were zoned for good public middle schools, "they knew which roads you don't want to live on because the traffic is heavy." He added, "It was like getting an insider's perspective."

After ruling out Westchester because of high taxes, they narrowed their search to Old Greenwich for its "proper Main Street," good schools and proximity to the water.

March 11, 2016

Trulia maps for choosing a neighborhood

Educated yet ? Via trulia.com/local/.

Northern Queens, how good it is ? Flushing, East Flushing, Murray Hill, Auburndale, Oakland Gardens ?

January 21, 2016

FDIC's Signs of predatory lending

Signs of predatory lending include the lack of a fair exchange of value or loan pricing that reaches beyond the risk that a borrower represents or other customary standards.

- Furthermore, as outlined in the interagency Expanded Examination Guidance for Subprime Lending Programs,1 "predatory lending involves at least one, and perhaps all three, of the following elements:

Making unaffordable loans based on the assets of the borrower rather than on the borrower's ability to repay an obligation;

- Inducing a borrower to refinance a loan repeatedly in order to charge high points and fees each time the loan is refinanced ("loan flipping"); or

- Engaging in fraud or deception to conceal the true nature of the loan obligation, or ancillary products, from an unsuspecting or unsophisticated borrower."

January 16, 2016

Caliber mortgage loan modification

Lone Star and its Caliber unit have become a magnet of criticism from housing advocates and housing lawyers who complain that the companies are too quick to foreclose on delinquent borrowers or to refuse to negotiate with borrowers over terms of plans to make loans more affordable.

The private equity firm's practices in dealing with delinquent borrowers was the subject of a recent front-page article in The New York Times.

In particular, critics have taken issue with Caliber's standard loan modification that temporarily reduces a borrower's payments for five years but then reverts back to the original payment terms in the sixth year, often with all the deferred payments added to the back end of the loan. The critics contend the temporary modifications merely enable Caliber to begin collecting payments on a loan that has been delinquent for many months or years, but provide no permanent relief to a borrower whose income has declined because of a financial crisis.

Ellie Pepper, an employee of the Empire Justice Center and regional coordinator for the attorney general's homeownership protection program, said the center had worked with a number of borrowers who have been presented with a temporary five-year loan modification from Caliber.

January 9, 2016

KonMari: Philosophy of household goods at rest or in service

Discard everything that does not "spark joy," after thanking the objects that are getting the heave-ho for their service; and do not buy organizing equipment -- your home already has all the storage you need.

She proposes a similarly agreeable technique for hanging clothing. Hang up anything that looks happier hung up, and arrange like with like, working from left to right, with dark, heavy clothing on the left: "Clothes, like people, can relax more freely when in the company of others who are very similar in type, and therefore organizing them by category helps them feel more comfortable and secure."

Smaller, English-only under-titles:

Such anthropomorphism and nondualism, so familiar in Japanese culture, as Leonard Koren, a design theorist who has written extensively on Japanese aesthetics, told me recently, was an epiphany to this Westerner. In Japan, a hyper-awareness, even reverence, for objects is a rational response to geography, said Mr. Koren, who spent 10 years there and is the author of "Wabi-Sabi for Artists, Designers, Poets & Philosophers."

Continue reading "KonMari: Philosophy of household goods at rest or in service" »

January 7, 2016

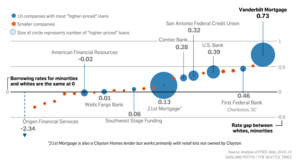

Clayton Homes vs Buzzfeed, Part 3

Seattle Times' business' real estate's minorities exploited by Warren Buffett's mobile home empire -- Clayton Homes.

Mike Baker and Daniel Wagner write in The Seattle Times / BuzzFeed News.

Compared to peers, Vanderbilt charges minorities the most

Under federal rules, a lender making a "higher-priced" loan must disclose data about its interest rate. Among the 25 companies that originated at least 500 such mobile-home loans over the past five years, Clayton Homes' Vanderbilt Mortgage gave the highest rates to minority borrowers as compared to whites.

January 4, 2016

Clayton Homes 2

2. Single Parent Programs:

assets.documentcloud.org/documents/2650256/Gonzales-Single-Parent-Loan-Ad.pdf.

Previously: 1: Clayton Homes vs Buzzfeed

January 3, 2016

Clayton Homes vs Buzzfeed

Reporting Mischaracterizes Clayton Homes' Treatment of Customers and Employees

Company Serves Underserved Markets, Making Homeownership Affordable

We categorically and adamantly deny discriminating against customers or team members based on race or ethnicity as Dan Wagner and Mike Baker insinuate in an article published by The Seattle Times and BuzzFeed. In fact, our company is committed to building on our track record of helping individuals and families from all walks of life, including people in historically underserved markets, achieve the American dream of home ownership.

Gawker chimes in.

Next:

December 29, 2015

Branding and the SOHO neologism: Solo District by Appia Group

'At the corner of Lougheed Hwy and Willingdon Ave, Burnaby, BC' or 'SOLO' South of Lougheed ?

Solo District by Appia Group offers aspirational branding for their planned mixed use infill community development.

Included with the first building is a Whole Foods store, which, if history is prologue, bodes well for Solo District and the surrounding area. In the U.S., they call it the Whole Foods effect: wherever the Texas-based organic food chain locates a store, prices for surrounding real estate jump. The debate continues over whether those prices rise because of Whole Foods' presence, or because the chain is good at selecting markets where the future is bright. In any case, no one questions that Whole Foods is a desirable amenity.

Continue reading "Branding and the SOHO neologism: Solo District by Appia Group" »

November 9, 2015

Millennial stealth dorms ruining Texas cities -- Citylab

Citylab reports millennial stealth dorms are ruining Texas cities.

Center: ZIP code 78751

In 2000, there were 3,723 higher ed students in 78751 (the area seemingly most affected by 'stealth dorms'). The total population in 2000 for 78751 was 14,005. So, the area was 27% students. In 2011, there were 4,760 higher ed students; the total population was 14,526. The area was 33% students. So, if you are a resident of 78751, of the sixteen people living closest to you one went from being a non-student to a college student. And by the way, four of the sixteen of them were already students. That is what is being described as 'bleeding' a neighborhood.

March 21, 2015

Mapping NYC's growth

Mapping how NYC's housing market spurs population change.

CHPC NY's making neighborhoods map.

November 9, 2014

Redfin chasing, catching Zillow

Some competitors like Redfin could one day assemble better data then Zillow because they have on the ground coverage and better data access through their network of real estate agents.

September 18, 2014

Where to live ?

Since 1950, the disparity between incomes and home prices has steadily widened to the point that many urban areas have become largely unaffordable to the middle-class workers who once inhabited them. Economists at the University of Pennsylvania and Columbia have coined the term "superstar cities" to refer to the likes of New York, San Francisco, Los Angeles and Boston. "Even large metropolitan areas might evolve into communities that are affordable only by the rich, just [like] exclusive resort areas," wrote the economists Joseph Gyourko, Christopher Mayer and Todd Sinai in a 2013 article.

As the superstar cities have become unattainable, the middle class is increasingly finding refuge in places like Philadelphia or Nashville, Denver or Charlotte, N.C. An example of "the people who are getting killed," Renn said, "is the old traditional blue-collar Queens person who's now getting squeezed with taxes and with housing costs. It's clear they don't fit into the vision of the city. They're basically realizing, Hey, I can go to Charlotte and live like a king on a truck driver's salary."

September 14, 2014

Tony or hip Bushwick wins two ways

Ryan Jensen, a stay-at-home father and part-time photographer with a second child on the way, was priced out of East Williamsburg and now rents a three-bedroom in Bushwick that is about a 15-minute walk from the L train. "We're the leading edge of gentrification," he said. "We're the people willing to be in these areas where there isn't transportation, or where our kid may be the only white kid in the school, or where there aren't amenities. We have delis, and that's about it."

September 7, 2014

China's Campaign to Turn Working Women into Wifeys

Passport

China's Totally Misguided Campaign to Turn Working Women into Wifeys

Why China's leaders would want to push a generation of professional women back into the home at a time when Japan and South Korea are desperately trying to leverage the economic potential of women workers. At the World Economic Forum in January, for example, Prime Minister Shinzo Abe noted that increasing women's labor participation could boost Japan's GDP by as much as 16 percent. Other studies suggest that restricting job opportunities for women costs Asia $46 billion a year.

The answer, argues sociologist Leta Hong Fincher, lies in the Chinese government's determination to maintain social order at all costs, a subject she explores in her forthcoming book, Leftover Women. The book's title refers to a pejorative term, sheng nu, used by the government to describe unmarried women in their mid- to late-20s. Fincher argues that the "leftover women" campaign -- comprised of media propaganda, mass matchmaking events, and bogus studies about the debilitating effects of singledom -- are one piece of a larger state effort to control women, and society, through economic and cultural means.

July 31, 2013

Middle class is $140k for NY renters

Davidson admits that eliminating rent controls would likely drive everyone who makes less than $90,000 out of Manhattan, which he says would not be healthy for the city, but then he claims that it would be "great" for the middle class. This makes sense if he's defining "middle class" as an income in the low-mid six figures, visualizing all the fantastically located apartments in Manhattan and brownstone Brooklyn occupied by rent-regulated peasants, and imagining that a mass eviction would open up many more choices on the market and might even enable him to snag a place for $3,300 instead of $3,750.)

Curiously, the real-estate lobby has yet to advocate for the tax increases necessary to adequately fund the federal Section 8 rent-subsidy program, which has been closed to new applicants here since 2009 and generally won't help pay for a two-bedroom apartment that costs more than $1,474.

June 13, 2013

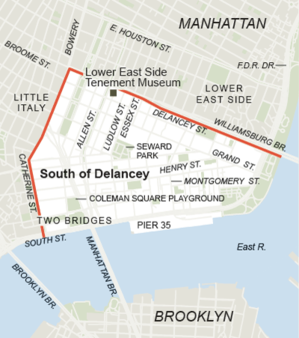

Lower East Side's south side is quiet

The Lower East Side, whose tenements teemed with immigrants for generations beginning in the 19th century, has in recent years become known north of Delancey Street for crowds of a different sort: the whooping revelers who stream down its streets and cascade from its scores of bars, restaurants and falafel shops on weekends. Indeed, the density of raucous nightspots has earned the nickname Hell Square for the area between East Houston and Delancey from Allen Street east to the Delancey, a club near Clinton Street.

Below Delancey, however, a quieter, more residential atmosphere prevails.

"When you cross south over Delancey you feel your blood pressure go down," said Para Rajparia, a psychologist, who moved into a three-bedroom Grand Street co-op in 2010 with her young family, joining the many other young professionals who have recently put down roots in the area. "I have a sense of safety and comfort."

Although new night-life attractions have begun pushing south down Ludlow Street from Delancey, they do not for the most part extend below Grand, leaving intact, at least for now, a certain low-key authenticity that many residents say they prize.

April 23, 2013

saving old buildings and neighborhoods is essential to the continued vitality of great cities

In the early 1990s, Shanghai organized a special economic zone that led to the development of a financial hub in Pudong, on land previously occupied by warehouses and wharves. Towers sprouted to create an instant iconic skyline, but with a regrettable, scaleless urban moonscape below.

Should we in New York in 2013 emulate the Shanghai of the 1990s? Or should we heed the lesson the Chinese themselves have subsequently learned, that saving old buildings and neighborhoods is essential to the continued vitality of great cities? In Shanghai, the pre-World War II buildings along the Bund, which loom so very large in the city's appeal, have been saved and repurposed. Nearby, at Xintiandi, a historic residential neighborhood of stone houses and tight alleys has been transformed into a chic, walkable retail and entertainment district.

Terminal City, a sophisticated mix of hotels, clubs, office buildings and residential blocks at the heart of East Midtown, was built on platforms bridging the rail yards north of Grand Central. It was a bold plan to create valuable real estate where once there had been urban blight. As much as anything, this development created what the world knows today as Midtown Manhattan.

-- Robert A. M. Stern

April 13, 2013

Co-ops rent some units for the benefit of all

A lucrative ground-floor lease can add 10 percent or more to the value of an apartment, residential brokers say. A sprawling two-bedroom loft at 464 Broome Street in SoHo, New York, for example, is in contract for $3.22 million, nearly 10 percent over its asking price, in large part because the listing not only offers no maintenance but provides its shareholders with $20,000 a year in income.

"The building has just eight apartments," said Henry Hershkowitz, a broker at Douglas Elliman who represented the seller, "so the revenues from the two stores on the ground floor cover the real estate taxes, the building's upkeep, even a full-time super, and then there is money left over for an annual dividend."

An apartment of this size in SoHo would typically come with a monthly maintenance of $2,400, said Robert Dankner, the president of Prime Manhattan Residential, which represented the buyer. When $20,000 a year in dividends is added to the nearly $30,000 saved in maintenance, there is a net savings of close to $50,000 a year, he noted.

As Mr. Dankner put it: "Depending on how you model it, it would take $750,000 earning a 6.5 percent interest to get that kind of return. Or, if they live there for 10 years, they save themselves half a million dollars. If you think of it from this perspective, even with the bidding war and it selling for over ask, the apartment was undervalued."

Continue reading "Co-ops rent some units for the benefit of all" »

March 27, 2013

Clean as I've been

In the flowering of modernism between the end of the First World War and the beginning of the Second, architects forged a stainless-steel connection between housing and health. Victorian homes were a nightmare to them, a cesspit at any level of society: they were dark and stuffy; they were filled with carpets and hangings and ornate picture frames that harbored dirt and were difficult to clean; their primitive plumbing made it hard to bathe.

See Light, Air and Openness: Modern Architecture Between the Wars

By Paul Overy, reviewed by Edwin Heathcote.

The early modernists wanted to wash away this squalor with an ocean of shining chrome, tile and white plaster. Dirt-hoarding fabrics with grime-concealing patterns would be consigned to the efficient rubbish chutes. Furniture would be made from wipe-clean leather and steel. Generous windows and electric light would expose every speck of dirt. In "Light, Air and Openness," the architectural historian Paul Overy showed how the early modernists were obsessed with healthful living and influenced by the design of sanitariums.

The better home would lead to better people. Love of purity, in the words of the Swiss architect Le Corbusier, "leads to the joy of life: the pursuit of perfection." He was far from the first to tie minimalist hygiene in the home to moral purity. Adolf Loos famously connected decoration with degeneracy in his 1908 essay "Ornament and Crime." A person's soul could be cleansed only when his domestic surroundings were purged: "Soon the streets of the town will shine like white walls. ... Then fulfillment shall be ours."

March 23, 2013

Brooklynites, priced out of Williamsburg, Boerum Hill, Carroll Gardens and Park Slope, are heading farther in. They are turning to neighborhoods like Sunset Park, Crown Heights, Bushwick and Prospect-Lefferts Gardens,

Many Brooklynites, priced out of Williamsburg, Boerum Hill, Carroll Gardens and Park Slope, are heading farther in. They are turning to neighborhoods like Sunset Park, Crown Heights, Bushwick and Prospect-Lefferts Gardens, bringing a willingness and an ability to pay more for housing than the waves of residents who came before them.

"What many clients have told me is that they like the old Brooklyn vibe of these up-and-coming areas," said Kristen Larkin, an agent with TOWN Residential. "They like the sense of community, friendliness of the neighbors, and the mom-and-pop shops that come along with it.

March 18, 2013

Real Estate title insurance: competitive ?

Title insurance rates vary considerably by state. In New York, insurers belong to a rating bureau that submits a rate schedule for state approval. Depending on the value of the property, costs can easily run into the thousands. On a $500,000 home with a $400,000 mortgage, for example, the premium in the New York City area would be $2,666, according to Rafael Castellanos, the managing partner of Expert Title Insurance Agency in Manhattan. "It's a bargain in the end given the protection title insurance provides," he said.

Yet for years, a debate has raged as to whether premiums are too high, competition too constrained, and the insurers too closely intertwined with the mortgage and real estate professionals who send business their way. Some states have looked into the arrangements between title insurers and referral sources, including New York. In 2006, two title insurers that account for half the New York market -- the Fidelity National Title Group and First American -- agreed to 15 percent rate reductions to settle state allegations of illegal referral payments and rebates.

Continue reading "Real Estate title insurance: competitive ?" »

March 11, 2013

Brooklyn Investor Loews $$L

Taxes: Oh yeah, and I haven't assumed any taxes on the above calculations. In recent years, unrealized gains seems to be offset by losses (note the deep discount to book value of CNA). So it would be a wash. Plus, these folks tend not to pay taxes. I think any monetization will come through spinoffs, exchanges and other tax efficient means. Part of the discount in L stock might be due to people applying 20% discounts to the value of publicly listed holdings for tax and liquidity. It may be the correct way to look at things, but I'm not convinced enough to put it in my valuations.

Conclusion: Anyway, this L is a really boring stock

Brooklyninvestor's Loews adjusted book value update.

Part 2 is up.

March 9, 2013

New amenity : linear drains

The residences will offer custom features like linear drains in showers (so the water rushes out faster), kitchen countertops with marble mined in Alabama, and design elements like a raised medallion on the walls of the bathrooms. There will be parking for 92 vehicles, 15,000 square feet of amenities in the basement (including a 75-foot pool), and two gas-powered generators with submarine doors on top of the building, which were added to the designs after Sandy.

The development also has 10 attached town houses, ranging from $8.75 million to $12.25 million, five of which have private garages. All but two are under contract. A five-bedroom duplex penthouse, with 2,500 square feet of outdoor space, is currently available for $35 million.

The sales velocity at 150 Charles has stunned all involved and created a mad scramble to adjust to the demand. Since Feb. 12, the development has raised the price of its offering plan nine times to $785.67 million, a boost of nearly 13 percent. (56 Leonard Street has raised prices three times, by a total of 4 percent.)

Still, 150 Charles is not beloved by all its neighbors. A group of West Village (NYC) residents is still fighting to stop the development, claiming the developer unlawfully tore down the original building at the site. They wanted Mr. Witkoff to construct a taller, narrower building (up to 32 stories), which he had the right to build, that would have blocked fewer views and allowed in more light. He chose instead to construct a shorter, wider building, supposedly because it was more in keeping with the character of the Village.

February 24, 2013

Land in New York is worth more today than at the peak of the market in 2007

Land in New York is worth more today than at the peak of the market in 2007, Mr. Knakal of Massey Knakal, a New York property sales company said. While the average price per square foot for a building lost 38 percent of its value from that time, the average price per square foot for land fell only about 18 percent, he said. Why the discrepancy? Not much land was for sale in 2009 and 2010, as sellers decided to ride out the market downturn and hold on to less sought-after sites, he said.

That has changed rather drastically in the past year with the surge in the number of development sites being sold. The big sales have not been confined to Manhattan. Last year Mr. Knakal brokered the $54 million sale of a 2.19-acre South Williamsburg, Brooklyn site zoned for residential units. The buyer was the government of China, in what Mr. Knakal said he believed was the first such transaction by a foreign-based buyer outside of Manhattan.

December 8, 2012

Real estate recovery in diversified cities.

Q. How would you categorize 2012?

A. Coming out of the recession the big gateway cities were the ones that performed best. That included New York, Washington, San Francisco, Boston, Chicago and Los Angeles. That's where investors were willing to take risks. You had diverse employment base, better leased buildings, less risk of a double-dip micro recession.

So that's where we were -- and 2012 was a continuation of that.

Apartments were the darling real estate subsector. But what happened in 2012 was we saw apartment cap rates get too low in some of those markets -- south of 5 percent -- and so investors were looking to invest outside apartments and outside the gateway cities. We started seeing in 2012 an interest in the office asset class, the industrial asset class, and a little bit more interest in retail.

Q. Are there regions of the country where you see future growth?

A. The other 45 markets that are covered in our investors survey look like that's where all the opportunities are -- whether it be Raleigh-Durham, N.C.; Texas markets like Austin, Houston and Dallas; Seattle; and Denver.

None of them is radically overbuilt from an office or apartment perspective. What's also interesting is those markets have a high percentage of echo boomers in their population -- the 25- to 34-year-olds. That's who's going to buy a house in the future, who's going to work in an office or retail or warehouse, or shop in retail

Continue reading "Real estate recovery in diversified cities." »

November 18, 2012

Marketing new condos in the best light

THE SQUARE FOOTAGE There are myriad ways to determine the square footage of an apartment. Some developers measure from the exterior walls, which adds unusable space to the figure. Others include outdoor space like a balcony, part of the exterior hallway or storage space -- even if the storage unit is in the basement. "That can add anywhere from 10 to 40 percent to a plan," said Dolly Lenz, a high-end broker at Prudential Douglas Elliman. "It's really problematic." To avoid ending up with a unit smaller than indicated in the marketing materials, make sure you understand exactly how your apartment is measured.

September 3, 2012

b2b2c Zillow: how b2c becomes also b2b

Consumer Internet companies of the newer generation are doing even more. In many cases, the tools they are providing businesses resemble specialized versions of so-called customer relationship management services from companies like Salesforce.com, which help businesses increase sales and keep track of communications with clients.

By moving in this direction, consumer Internet companies hope to tap potentially rich new sources of revenue, which could make them more attractive to investors. A company that gets business clients to depend on a broad set of its services can make it tougher for competitors to swipe its customers.

"You can't just sell advertising without being exposed to someone else undercutting you on price," said Spencer Rascoff, chief executive of Zillow. "If you sell ads plus services, you're in a more defensible position."

Bill Gurley, a Zillow board member and venture capitalist, has seen enough hybrid Internet companies that serve both businesses and consumers that he coined a term to describe them: B2B2C. "We're moving from a day and age where you're just a Web site to one where we're automating the connections between businesses and consumers," he said.

Mr. Gurley's firm, Benchmark Capital, has invested in several other companies he puts in that camp, including Uber, which offers a mobile app that lets consumers hail a town car and gives drivers a "heat map" highlighting the areas where they are most likely to find customers.

GrubHub, another one of his investments, lets consumers order takeout and delivery food from more than 15,000 restaurants online and through mobile apps. In many cases, the service uses a clunky system in which customer orders are sent to restaurants by fax and confirmed by phone.

Recently, though, GrubHub introduced a product called OrderHub that could allow it to become more entwined in restaurants' operations. OrderHub is a tablet computer running Google's Android operating system that lets restaurants receive orders electronically, confirm them with a couple of taps and improve the accuracy of delivery time estimates.

July 22, 2012

Tall building of New York: the first three centuries

These were buildings no taller than the Dakota, but in 1885 The New York Times urged restrictive legislation and darkly predicted that "if the streets were lined with eight-story buildings, half of the occupants would be deprived of sunlight, and their children would be etiolated like plants grown in a cellar." You can tell it's serious when The Times brings the kids into it.

As tall buildings grew in numbers, architects found themselves in a difficult position. In 1894 the prominent architect George B. Post denounced the skyscraper, as it was now freely called, as an "outrage." On the other hand the commission he received from his $2 million, 10-story New York World Building, on Park Row -- well, that put outrage in a certain perspective.

In 1897 The Record and Guide, alarmed by a proposal for a building 2,000 feet high, protested that New York was open "to attack from the audacious real estate owner" who cared nothing about robbing light from the neighbors, adding, "All that is needed is a barbarian with sufficient money and lunacy." The Chamber of Commerce, equally alarmed, supported legislation to severely restrict skyscrapers.

July 21, 2012

I think they meant downpayment

Renters don't have to lay down massive deposits, suffer the headache of dealing with condo and co-op boards, or pay taxes, common charges and big repair bills after signing away their savings.

June 20, 2012

Brooklyn is booming

June 10, 2012

Sod on top: green roofs save energy, sewage

Putting living vegetation on the roof is not a new idea. For thousands of years people have made sod roofs to protect and insulate their houses, keeping them cooler in summer and warmer in winter. The modern movement for green roofs began in the last 50 years in Europe. Germany, where about 10 percent of roofs are green, is the leader; some parts of Germany require green roofs on all new buildings.

Greening a roof is not simple or cheap. Over a black roof -- flat is easiest but sloped can work -- goes insulation, then a waterproof membrane, then a barrier to keep roots from poking holes in the membrane. On top of that there is a drainage layer, such as gravel or clay, then a mat to prevent erosion. Next is a lightweight soil (Chicago City Hall uses a blend of mulch, compost and spongy stuff) and finally, plants.

An extensive roof -- less than 6 inches of soil planted with hardy cover such as sedum -- can cost $15 per square foot. An intensive roof -- essentially a garden, with deeper soil and plants that require watering and weeding -- can double that. But because the vegetation is thicker, it will do a better job of cooling a building and collecting rainwater. Plants reduce sewer discharge in two ways. They retain rainfall, and what does run off is delayed until after the waters have peaked.

Continue reading "Sod on top: green roofs save energy, sewage" »

May 17, 2012

Price negotiation with real estate developers

GAME PLAN

The New York real estate market has tightened this spring, but buyers can still get good deals on new condos. Following are some tactics you might consider:

BE FIRST Developers want to kick-start sales to generate momentum, and they also need to sell a certain percentage of units to qualify the condominium as a functioning business entity.

BE LAST Especially if a project has been on the market for many months, the developer and brokers may offer discounts or incentives to unload the final few units.

ON THE MARGINS Smaller developments in emerging or out-of-the-way neighborhoods can be harder to sell. But if they meet your needs, there are bargains to be had.

BRING CASH Buyers who don't need financing contingencies in their contracts are a developer's dream.

RESPECT THE ASKING PRICE Developers are loath to offer price discounts because they lower the value of all other units. Instead, ask if some closing costs or legal fees could be covered.

May 9, 2012

Rogue HOA in Las Vegas

When a new development was nearing completion, the group would buy a couple of units in the community and then transfer partial ownership of the condos to individuals secretly on its payroll, according to court documents. While pretending to be residents of the communities, these "straw buyers" would run for leadership positions on boards of the new homeowner associations.

By paying off community managers, hiring private investigators to find dirt on legitimate candidates and rigging elections, the documents allege, the straw buyers were able to infiltrate boards at several new developments in Las Vegas from 2003 to 2008. Once in control of the boards, the straw buyers would then use their governing positions to steer millions of dollars in construction and legal fees back to their co-conspirators. Targets included the Chateau Nouveau, Chateau Versailles, Park Avenue, Palmilla Townhomes, Jasmine, Pebble Creek, Mission Ridge, Mission Pointe, Horizons at Seven Hills, Sunset Cliffs and the Vistana.

-- Felix Gillette, Businessweek

May 5, 2012

Housing in better school district costs a $11,000 a year

A new study from the Brookings Institution quantifies that price gap, and the differences between the cost of living near a high-scoring public school and a low-performing one are striking.

The study, by Jonathan Rothwell, a senior research analyst in the Metropolitan Policy Program at Brookings, found that housing costs in the nation's 100 largest metropolitan areas were an average of 2.4 times as high - a difference of $11,000 a year - for homes near schools whose average test scores put them in the top fifth of schools in the area, compared with schools in the bottom fifth.

That means that a family would have to pay more per year to move into a good public school zone than for their children to attend some private schools. Translated into an average home price, the gap works out to an average of $205,000 more for a home near a high-performing school.

"We think of public education as being free, and we think of the main divide in education between public and private schools," Mr. Rothwell said in an interview. "But it turns out that it's actually very expensive to enroll your children in a high- scoring public school." Mr. Rothwell said that in the New York metropolitan area, for example, annual housing costs are $16,000 higher on average in neighborhoods near high-performing schools than in neighborhoods near low-performing schools,

Continue reading "Housing in better school district costs a $11,000 a year " »

April 26, 2012

Tight credit keeps would-be owners renters

Real estate evidence that rising rents are driving perspective renters into the sales market. But for those who find buying a home in New York City is not an option -- whether because of bad credit, tougher lending standards or lack of a down payment -- the choices are limited and often unappealing.

Landlords and brokers say more and more young people are sharing, even if it means sacrificing a living room to add a bedroom or two. There has also been a surge of interest in the other boroughs, with many neighborhoods reporting record rents of their own.

Some tenants may be able to negotiate with their landlords, especially if they are long-term renters with good track records. But property owners have little reason to cut deals, because the vacancy rate in Manhattan is hovering around 1 percent.

And just 2,229 rental apartments are scheduled to be added to the market this year in Manhattan, a 30 percent drop from the average number over the last seven years.

The uncoupling of the national economy from New York rents is not typical, said Jonathan J. Miller, the president of the appraisal firm Miller Samuel. "When you see rents rising, it is usually reflective of a strong economy," he said. "That is not the case now."

Instead, he said, prices are being driven up by a tight credit market that forces people to stay in the rental market and limits new construction.

Continue reading "Tight credit keeps would-be owners renters" »

March 25, 2012

Harlem re-renaissance

Norman Horowitz, an executive vice president of Halstead Property who has sold several hundred properties over the last decade in Harlem, said, "Harlem was gentrifying before the recession, then there was a pause, and now the trend is picking up again."

Some experts caution, however, that a Harlem recovery could be destabilized if a backlog of foreclosed or distressed properties went on the market. While figures are hard to come by, "there is a lot of hidden inventory, where banks are just holding on to these units, but have yet to put them up for sale," said Willie Suggs, a well-known Harlem broker.

Some builders contend that prices are still too low to justify new development. "At $500 to $600 a square foot," said Michael K. Shah, the chief executive of DelShah Capital, a developer, "condo projects just don't pencil out yet." Prerecession condominium prices in Harlem were around $850 a square foot, he said, and until prices climb further, "there is just too slim a profit margin after factoring in the cost of construction and land -- I don't think you will see a lot of new development for at least another two to three years."

Still, some brokers and residents insist that this market rebound is meaningful.

The Downeses had been living in a three-bedroom condominium on West 119th Street for six years before their growing family created a need for more space.

"We looked all over the city," said Ms. Downes, an executive vice president of Pacific Investment Management Company, "but it was really hard to find any four-bedrooms for under $3 million." When they found the five-bedroom house around the corner on West 120th Street, they began a slow negotiation with the developer over the $2 million price tag.

"Then one weekend morning I was out walking my dog, and saw two couples looking at the house, talking about making offers come Monday," she said. "I went up to them and said, 'Oh, we are already in contract, that is my house.' " She and her husband, who works on Wall Street, quickly closed the deal and moved in earlier this year.

March 17, 2012

Home office

Live-work real estate: Most spaces advertised as "home offices" are alcoves or windowless rooms that cannot legally be called bedrooms. The New York State Multiple Dwelling Law says rooms for sleeping must have at least 80 square feet of floor space, no measurement less than 8 feet, and window area that measures at least 12 square feet and is also at least a 10th of the area of the room. There are also rules about how much space needs to be between the window and the next lot. In addition, there are exceptions to this rule for some older buildings, according to an official at the New York City Department of Buildings.

A room that falls outside these parameters is given another name -- media room, den, library, dining room -- but more and more these days it becomes the home office.

January 22, 2012

Bigger apartments for NYC

Mr. Walsdorf said that when Flank began selling condos at 385 West 12th Street, a building completed last year, buyers were interested in combining the smallish units, and "we hadn't really allowed for that possibility in the layouts." This time the firm decided to build large units and stuck to it, even after the financial collapse of 2008. (VillageCare, which operated the nursing home, agreed to sell the building in 2007 but was unable to move out until 2009.)

The conversion of public or institutional buildings into upper-class housing has a long history in New York. The former police headquarters at 240 Centre Street is a condo building, as are the former Y.M.C.A. on West 23rd Street and several former school buildings around the city. The onetime New York Lying-In Hospital, at 305 Second Avenue, is the Rutherford Place condos.

To housing advocates, those conversions represent a victory for the wealthy. Jerilyn Perine, the executive director of the Citizens Housing and Planning Council, an advocacy group, said it was important that the city adopt regulations "so that denser housing, particularly for singles, has a fighting chance in the market." She added, "It's great to have people with a lot of money living here -- we need their taxes and spending power -- but the loss of density is tragic, especially where mass transit access is so great."

But at least in the case of the Village Nursing Home, the rich will not be the only beneficiaries. A few years ago, residents there were crammed into outdated rooms that averaged less than 300 square feet per person (current regulations require at least 500). VillageCare was able to build a more modern facility, the VillageCare Rehabilitation and Nursing Center at 214 West Houston Street, using money from the sale of the Hudson Street building. A spokesman for VillageCare, Lou Ganim, said residents remaining in the Village Nursing Home at the time it was sold were transferred to the new facility.

Indeed, sometimes preservation advocates look to condo developers as white knights. Since the Bialystoker Center for Nursing and Rehabilitation on East Broadway closed last year, Laurie Tobias Cohen, the executive director of the Lower East Side Jewish Conservancy, has been "extremely eager" for a developer to buy the historic building and convert it to co-ops or condos. The closing of the nursing home was a great loss, she said; the goal now is to prevent the demolition, or further deterioration, of the building. "What we don't want," she said, "is to lose any more of the built historic fabric."

January 21, 2012

Commercial Real Estate (Re-)Finance, NYC Offices 2007-2012

Some deal detail:

Instead of foreclosing on the 39-story building, which stretches from 52nd Street to 53rd Street, the lenders agreed last month to reduce the principal and defer some of the interest payments on the interest-only loan and extend its maturity for two years, until February 2019. In exchange, Kushner and its powerful new partner in the deal, Vornado Realty Trust, agreed to pour tens of millions of dollars into the building to improve its leasing prospects. The 1.5-million-square feet office building is currently 30 percent vacant.

Continue reading "Commercial Real Estate (Re-)Finance, NYC Offices 2007-2012" »

January 15, 2012

Liquidspace

Liquid Space is like an AirBnB for coworking space and real estate: blog.

Big in San Francisco, California and NY.

January 8, 2012

Lighting apartments

"You want to maximize the amount of times that daylight bounces inside the room," Mr. Tanteri said. To do so, he suggested using light colors that are "close to white" on ceilings, walls and floors, and avoiding glossy finishes. "Glossy surfaces can actually be a detriment because they can create glare," he said. "The safest finishes are matte finishes, because they reflect light in all directions."

¶ Mr. Steinberg also recommends using light hues, and offered specific paints. "Linen White by Benjamin Moore is a very reliable, sell-your-house coat of paint," he said. He suggested another Benjamin Moore color, Decorators White, for the ceiling and trim.

¶ On a related note, Mr. Tanteri said: "You don't want to cover the wall with dark hangings. Paintings and posters will absorb light."

¶ As for reducing light obstructions, "Orient objects in the room to promote the flow of daylight," he said. "So, things like bookshelves and partitions should be perpendicular to the window wall."

¶ Mr. Tanteri also says that light from the top of a window will reach the farthest into the apartment, so it is important not to block that part of the window with heavy blinds or drapery.

¶ He favors Venetian blinds because they provide solar control and can also redirect sunlight to the ceiling. "That's when you get deeper daylight penetration," he said. Another option: shades that travel from the bottom of the window upward, rather than top down. "That's something that works for daylight as well as privacy," he said.

¶ And you can supplement the sunlight with strategically placed light fixtures. "Use indirect lighting, aimed at the ceiling," Mr. Tanteri said. A torchier floor lamp near the back of the room could "take over where the daylight on the ceiling starts to fade away."

December 10, 2011

Affordable housing and people can't afford it not coming to Darien, yet.

One remark was taken from a 2008 hearing on another affordable housing application, in which Mr. Conze referred to such housing as "a virus" that needed to be contained.

The other is from his State of the Town Address last December, when, speaking of the trend toward development of high-density housing along transportation corridors, Mr. Conze warned, "The demographic and economic forces generated by our immediate neighbors to our east and west cannot be taken lightly," adding that many people "view Darien, CT, as a housing opportunity regardless of its effect on the character of our town and existing home values."

Darien's neighbors to the east and west are the cities of Norwalk and Stamford. Mr. Hamer's complaint contrasts the 0.5 percent of Darien's population that is black with the roughly 22 percent in the bordering cities.

Continue reading "Affordable housing and people can't afford it not coming to Darien, yet." »

September 21, 2011

Montclair, NJ

In Montclair, NJ, where there is a concerted emphasis on thinking of the town as one diverse whole -- children are bused to "magnet" schools, and the moniker "Upper" is discouraged as divisive -- several agents resisted comparisons of trends on the two sides of town.

"Sometimes people come in saying they only want to buy in the one ZIP code, 07043," said Linda Grotenstein, an agent at Coldwell Banker. "I usually find they have a misunderstanding of what the ZIP codes imply."

The housing stock is more homogeneous in the northern half: mostly well-groomed Victorians with three to six bedrooms. The south end has far greater range: everything from run-down, run-of-the-mill triplexes on narrow lots to peerless mansions on manicured grounds, in the "estate section."

In fact, by Mr. Baris's reckoning, the estate section in the southern part of Montclair has kept overall average sales value afloat. It had 42 listings this year, and 18 houses sold, at a median price of $1.218 million, 31 percent more than last year.

"If you took out the estate section," Mr. Baris said, "Montclair would have depreciated as a town."

In Millburn/Short Hills, Ms. Bigos ascribes the huge price disparity to the teardown craze that swept Short Hills starting in the late 1990s.

"That is when the spread started to widen," said Ms. Bigos, a lifelong resident of Short Hills. "All the new houses going up doubled and tripled in value."

Both Millburn and Montclair have Midtown Direct New Jersey Transit train service to Manhattan, which various reports have shown can increase property value by as much as 20 percent. Millburn has had it for 15 years, while the service arrived in Montclair seven years ago.

July 17, 2011

New houses look old but offer utility and green features

IVY is creeping up the walls of the stone neo-Georgian Revival-style manor house on the harbor here. Towering old oak and pine trees and a 35-foot blue Atlas cedar punctuate its lushly landscaped lawn. The seven-bedroom residence, with arched dormers, a columned portico with a fluted cornice design, transom windows, a slate roof and a widow's walk with a Chippendale railing, looks as if it has been there for a century. It was finished last summer.

On an island where the traditional is king, most residences can easily be dated -- Capes to the postwar Levittown era; ranches, split levels and then high ranches in the '50s and '60s, cedar-sided contemporaries in the '80s, and during the McMansion boom in the late '90s, "colonials on steroids."

Over the last decade, many architects and builders have veered toward a more ageless, classic approach.

Continue reading "New houses look old but offer utility and green features" »

July 16, 2011

Condo owners are screened, too

In the downturn, many owners stopped paying common charges, and condominiums had little recourse to recoup their money. In case of a default, the city is first in line to recover outstanding real estate taxes or other charges, followed by the mortgage lender. The condominium is third in line, and usually all it can do is file a lien against the property and hope that it will be repaid when the apartment is sold.

Because the condominium's power is limited, it is a matter of fiduciary duty to find strong buyers, said Carl Seligson, the board president of Carnegie Hill Tower, at 40 East 94th Street. In any given month, about three apartments in the 180-unit building have not paid their monthly charges on time; none have defaulted, he said.

July 14, 2011

Screening tenants for credit and income

Most landlords in NYC require a lot of information. They want to see a prospective tenant's tax returns, pay stubs, bank statements, proof of employment, photo identification, and sometimes, reference letters from previous landlords. Everyone will run a credit check (many Manhattan landlords look for a score above 700) and just about all, from big management firms to small-time landlords, want to know that your gross income is somewhere between 40 and 50 times the monthly rent.

Using that formula, someone renting an apartment for $3,000 a month must earn at least $120,000 a year.

"It mirrors the requirements used to qualify you for a mortgage," said Scott Walsh, the director of market research at TF Cornerstone, a property management and construction firm in Manhattan.

Apartment hunters should be ready to produce all of these documents. And, said Steve Maschi, a vice president of Glenwood, a Manhattan property management firm, prospective tenants should be ready to write a check on the spot for the first month's rent, the security deposit (usually a month's rent) and if a broker is involved, that fee (8 to 15 percent of a year's rent).

Those who lack the required income or credit score, or those relocating here from overseas, may be shut out.

One recent apartment hunter, Sara Davar, said she was shocked when she ran into these hurdles. Ms. Davar, 28, an area director for Meltwater Buzz, which provides analytic tools for social media, had lived in her native Stockholm, as well as in London and in Philadelphia, and had not encountered anything like the requirements here. The stumbling block for her was the same as that encountered by most foreigners: no credit history in this country. Without it, no landlord would consider her.

Continue reading "Screening tenants for credit and income" »

July 3, 2011

Upper class rent starts at $10,000 per month

Do middle class apartments cost up to $10,000 per year ?

On the Upper East and West Sides, he said, there is strong interest from families for apartments with several bedrooms. His downtown clients, who typically work in the creative industries, tend to value location and design over space and even amenities, he said, and expect Sub-Zero or Viking appliances and remote-controlled sound systems and window coverings.

Other five-figure rentals offer a number of amenities. At 15 Broad Street in the financial district, James Cox of Prudential Douglas Elliman is marketing an apartment he described as being at the "low end of the high-end rental." At $12,000 a month, the two-bedroom apartment has almost 1,900 square feet of interior space, but its real draw is the 1,200-square-foot terrace with sweeping views of Lower Manhattan, Midtown and beyond. That, and the building's extras, like a single-lane bowling alley, basketball court, gym and pool in the basement and a billiards room, party space and parklike common terrace on the seventh floor that offers a full-frontal view of the frieze over the New York Stock Exchange.

As prices rise, so do the expectations, said Dennis R. Hughes, a senior vice president at Corcoran Group Real Estate. For about $20,000, he said, he was able to find one client, a divorced businesswoman moving from a town house, a 2,300-square-foot, three-bedroom apartment in TriBeCa with outdoor space and views of the Hudson River. For $45,000, a renter could have a 4,500-square-foot, five-bedroom apartment in a prewar doorman building on Fifth Avenue with a spa in the basement.

And for $85,000, Prudential Douglas Elliman is marketing a full-floor loft at 25 Bond Street with 7,326 square feet inside, five bedrooms, six and a half baths, fireplaces and terraces. It even comes with a movie star, Will Smith, staying just below.

Continue reading "Upper class rent starts at $10,000 per month" »

July 1, 2011

Sidewalks cost $100 per square foot

"It is an oxymoron," Adrian Benepe, the parks commissioner, conceded in an interview last year when the pilot project was being considered. "But boardwalk has become eponymous, in the way Kleenex is for paper tissue. It is a generic term for an elevated oceanfront walkway, and other communities use concrete."

About three weeks ago, the community board voted 21 to 7 against the latest compromise: running a 12-foot-wide concrete lane down the middle of the 50-foot-wide boardwalk to accommodate the wear and tear of garbage trucks and police cars. The remaining sides would be built out of planks made of recycled plastic that cost about $110 a square foot and last for years.

He also remembered that the Coney Island Boardwalk -- officially known as the Riegelmann Boardwalk for the borough president who built it as a way of offering the public greater access to the beach -- withstood storms like Hurricane Donna in 1960 relatively unscathed, while a concrete esplanade in nearby Manhattan Beach was mangled.

But concrete had its advocates, like Mila Ivanova. Ms. Ivanova, a Ukrainian immigrant to Brooklyn from Odessa on the Black Sea who also walks the Boardwalk every day, said: "It's very good -- wood -- but it's old. It is shaking. Sometimes nails come up and you fall. Personally, I like everything new."

June 26, 2011

Hamilton Heights to rise under Columbia ?

In the 1980s she lived on West 103rd Street in a one-bedroom co-op that she sold for $335,000 in 2002. Then, she said, Columbia built off-campus housing on her corner -- and in 2005 an identical apartment then sold for $500,000, which strikes Ms. Cabrera as a steep jump even in a hot housing market. She is now listing a four-bedroom 1901 town house at 470 West 148th Street for $975,000.

When the new Columbia campus is finished in 2050, Manhattanville will have a striking new look. Glass towers housing the business school, labs and classrooms will replace workaday brick structures, meatpacking warehouses and even a Studebaker plant. Sidewalks will be broadened and planted with trees. The $7 billion project -- designed by the architectural heavyweights Renzo Piano; Skidmore, Owings and Merrill; and Diller Scofidio & Renfro -- will create 6,000 permanent jobs, the university says.

Continue reading "Hamilton Heights to rise under Columbia ?" »

May 28, 2011

Discounted realtor commissions for discount service

Keith Burkhardt, the president of the Burkhardt Group, charged the Pohls a flat rate of $1,000 to submit their listing to real estate databases. The couple handled all the open houses, showings and deal negotiation themselves. He offers buyers a rebate of up to two-thirds of his commission, based on a similar self-service model. Clients search for apartments and visit open houses on their own, putting Mr. Burkhardt's name down as their broker, and he helps out by booking other appointments and offering advice during negotiations.

These days, Mr. Burkhardt considers himself mostly a buyer's broker, describing his niche as that subset of real estate enthusiasts who are glued to sites like StreetEasy and don't need a lot of hand-holding while visiting Sunday open houses, a task that can take up a lot of a broker's time.

"They're doing, let's say 60 percent of the research themselves," he said, "and they want to be compensated for that."

He acknowledged, however, that setups like his had yet to catch on in a big way.

"People like to complain about broker commissions," he said, "but they're afraid to break ranks with the status quo and go with a firm or a model that is different than what everybody accepts."

Another company offering a hybrid service is RealDirect, which charges sellers $395 per month, or a 1 percent commission, to distribute a listing to major real estate databases; owners handle open houses and showings themselves. Sellers can pay a 2 percent commission for what RealDirect calls "broker-managed service," including pricing and staging advice, and the handling of negotiations.

Doug Perlson, the chief executive of RealDirect, said 3 of the 13 apartments listed through the company, which started last summer, had sold or were in contract.

One of those properties is a one-bedroom Greenwich Village apartment owned by Colleen Gray, which is scheduled to close in mid-February. The listing price was $920,000.

Ms. Gray said she listed her apartment with RealDirect in late October after having tried to sell it herself for about a month. She went with RealDirect because she did not feel her previous real estate agents had earned their commissions.

Continue reading "Discounted realtor commissions for discount service" »

May 20, 2011

Home safe

D IVERSION safes, of course, are not fire resistant and do not even have locks. Their strength is pretense. They cost $5 to $100, and are designed to look like various household objects: a head of iceberg lettuce, a can of soda and a can of shaving cream. Cans, jars and aerosol containers found in pantries and bathroom cabinets are typical. These stealth safes also come disguised as other kinds of things, like surge protectors and clocks.

"They are great for hiding stuff like money and jewelry," said Annie Blanco, marketing coordinator for homesecuritystore.com, an online retailer of home security systems, based in Riverside, Calif.

But Paul Cromwell, a professor of criminology at the University of South Florida Polytechnic in Lakeland, who has interviewed scores of professional burglars in his research, said he is skeptical about their value. "Burglars are looking online at these kinds of safes, too," he said. "So they know what to look for."

Hiding valuables in coat pockets or shoeboxes, in the freezer or buried in the dirt of potted plants, he added, isn't any better. "You may think you're being clever, but these are the first places burglars look."

Criminologists and law enforcement officials also advise against putting things inside toilet tanks and cereal boxes (where addicts tend to hide illegal drugs) and inside medicine cabinets (where thieves look for prescription drugs with resale value). So the last place you want to hide your diamond necklace or a roll of bills is inside an empty bottle of Oxycontin or Adderall.

Apart from a steel-clad safe, he said, the best place to store valuables is one that would take a thief considerable time and effort to find.

"Burglars want to spend as little time as possible in your home," he said. "The average time a professional burglar will spend there is five minutes."

Good options might include putting what you want to protect in a nondescript box surrounded by a pile of junk in the attic, or tucking it into the stuffing of one of a group of stuffed animals.

May 15, 2011

Nanny rooms, servant's rooms

The Laureate, a new 20-story building at the corner of Broadway and 76th Street, NY has four such apartments -- each has four or more bedrooms and is priced at about $11 million. The maid's room is listed simply as another bedroom, but it is away from the others, closer to the front door and living areas. Two of the building's penthouse units even have separate entrances that lead directly to the servant's rooms.

Demand for family-sized apartments with separate quarters for live-in help has been so marked at the Laureate that the Stahl Organization, the developer, has decided to combine some smaller apartments to create more units that fit the bill, Mr. Reuveni said. Many of the interested buyers are coming from abroad, but others, he said, already live on the Upper West Side and are looking for homes that mirror the classic apartments in nearby prewar buildings. While the rooms could also be used as guest rooms or offices, most prospective buyers have said they will use theirs either for a live-in nanny or a housekeeper.

The apartments, listed for about $7.5 million each, are designed to feel like "a single-family home in the sky," Ms. Urgo said. "More and more parents are choosing to raise their children in Manhattan, and we have seen a need for these very large spaces." Many potential buyers have live-in nannies, "because people have full lifestyles and maybe you have two working parents," she added. "This type of apartment does fit a need."

Maid's rooms built in the 1910s and 1920s tended to be barely six to seven feet wide. Apartments that came equipped with them have three or more family bedrooms and might originally have had more than one maid's room. At 905 West End, the developer Samson Management took a Classic 8 -- which had three bedrooms, a living room, a dining room, a kitchen and two maid's rooms off of the kitchen -- and shifted and expanded the bathroom that had been shared by the maid's rooms, combining the remaining space to create one larger room.

April 30, 2011

Condos vs. co-ops: You can buy fashion. Style is something you earn

Nowadays, condo buyers tend to be foreigners, absentee owners, empty nesters and corporate types with an instant-gratification streak who want to put down as little as possible for flashy, turnkey residences that they also can get out of as fast as possible.

Co-op owners tend to be more "vested in New York," as Stribling's Kirk Henckels puts it--more social and financially stable, and more interested in the location and architectural quality (the steak, not the starchitect sizzle) that characterize Manhattan's best buildings, most of which are pre-World War II vintage co-ops around Central Park. Co-op buyers need "a different level of commitment," said John Burger of Brown Harris Stevens.

You can buy fashion. Style is something you earn.

Continue reading "Condos vs. co-ops: You can buy fashion. Style is something you earn" »

April 23, 2011

Whole Foods Market: leads or follows gentrification

But Christy Pardew, spokeswoman for Whose Foods, Whose Community?, an activist group protesting the forthcoming Whole Foods, says the issue is "keeping multinational chains out." According to Ms. Pardew, the addition of a high-end grocery store to Jamaica Plain will result in higher rents, pushing low-income residents from the neighborhood. "It's a term that real estate agents use," she intoned, "called 'the Whole Foods effect.'"

But real estate agents aren't economists, and Ms. Pardew admitted that there "isn't a lot of academic research" to back up the claim that stores like Whole Foods destroy low-income, ethnic communities. In fact, evidence points in the opposite direction: "To blame gentrification for rising rents is to get things exactly backwards," says Duke University economist Jacob Vigdor. "Companies like Whole Foods are building in places where the clientele is there already. They follow the customer."

When studying gentrification patterns in Boston, Mr. Vigdor investigated claims that elevated rates of neighborhood departure correlated with rising rents. "Actually, I found that in the gentrifying neighborhoods, the turnover rate among long-term residents was actually lower than it was in other parts of the city," because most residents see changes like lower crime rates and the revivification of derelict buildings as positive developments.

"People think that gentrification is causing prices to rise, when it's actually the reverse. In cities that are popular places to live, where demand exceeds supply, and prices go up all over the place--this leads people to seek out neighborhoods that are less expensive," says Mr. Vigdor.

Census data for Jamaica Plain show that Whole Foods is indeed following demographic trends, not simply hoping that if a store is built, the yuppies will come. In the past decade, the Hispanic population in J.P. has declined by 10%, while the African-American community shrunk by almost 15%.

Continue reading "Whole Foods Market: leads or follows gentrification" »

April 22, 2011

Old buildings of NYC

According to the 2008 Census housing survey, 85 percent of New Yorkers live in buildings erected before 1970, compared with 42 percent of Americans generally. More remarkably, 39 percent of New Yorkers live in buildings predating 1930 and 17 percent in buildings predating 1920. Luckily for New Yorkers with a taste for past lives, many of these dwellings function as palimpsests of the city's history.

April 8, 2011

Architecture critics detest Trump complex on Riverside South

Xanadu Mall in NJ is almost as bad a a Trump project.

In the New York region, "the only thing comparable would be Trumpville on the West Side Highway. It beats Xanadu in its sheer mass, and its brutal imposition on the eyes of millions of people."

MELISSA LAFSKY

Editor in chief of the Web site The Infrastructurist

I know various people have said the whole Trump complex on Riverside South is worse, and it is pretty bad."

PAUL GOLDBERGER

Architecture critic of The New Yorker

N.Y. / REGION

Fix Xanadu? The Problem May Be Where to Begin

By RICHARD PÉREZ-PEÑA

Published: April 1, 2011

Architectural experts offer thoughts on rescuing a stalled New Jersey Meadowlands mall project that has already soaked up $2 billion.

April 2, 2011

Nabewise beautiful

The Meat Packing District, SoHo, NoLiTa, and East Village are beautiful, according to NabeWise; see also NYC and SoHo pages.

Move on downtown.

March 20, 2011

Remodeling is not heavily financed

WHY THE REBOUND? It may seem counterintuitive that even as the housing market continues to suffer and the economic recovery feels tentative, the renovation market is picking up. But Mr. Baker pointed out that while home sales and construction were linked to mortgage rates, renovations were determined more by income levels and job security.

"Remodeling is not heavily financed," he said. Instead, people are willing to spend cash, Mr. Baker said, because they have "a comfort level that the value of my home isn't depreciating." -- Kermit Baker, director of the remodeling futures program at the Joint Center for Housing Studies.

He said during the peak years of 2006 and 2007, only 30 to 35 percent of renovations were financed through home equity loans or second mortgages. Last year, that number dropped to 15 to 20 percent.

March 17, 2011

Scarano's fun with NY zoning