April 14, 2016

November 3, 2013

Portfolioprobe's investment performance measurement vs calculation

Measurement as a call to action.

I said "measurement". My dialogist heard "calculation" but wanted "measurement". We went dizzy in the chase.

A calculation is what computers do.

A measurement is an assessment. It is a comparison with an ulterior motive.

I'm not going to weigh myself unless there is the possibility of a change in behavior. If there is no value of my weight that is going to affect the way that I act, then weighing is pointless -- the scale does the calculation but there is not actually a measurement.

Look at these on 4 schemes:

a performance statistic relative to a benchmark

a peer group

a performance statistic relative to no trading

random portfolios

May 13, 2013

"Sell in May and Go Away" means working only two days a year

The idea of the adage is that the markets tend to be weak during the six month period from May through October is something that hits close to home for investors, given that we have just turned the calendar to the month of May. As we look back over the past couple of years, we find that May has ushered in some choppy, if not sloppy market behavior. For example, in 2012 the market (as measured by the S&P 500 (SPX)) peaked in April and the slid roughly -10.6% by early June, pushed higher in the later Summer months, only to experience an -8% starting in October. Point being, the "weak period" in 2012 was filled with periods of "fits and starts." And we all remember 2011, as it truly tested investor's mettle, as the SPX dove -21% from its peak in May to its October bottom. Tack this on to 2010 in which the markets experienced the "flash crash" in May, and it's not surprising that recent memories of the markets from May through October have left a bad taste in investors mouths. This is not to say that all May through October time periods result in major corrections or seismic market events, but it is a period of time that the market has not historically made great strides.

So as we hit May and the beginning of the historically "seasonally "weak" period for Equities, now is the time to think about positioning your portfolios accordingly. "Tilting" seasonally, using a combination of low-volatility and Technical Leaders ETFs, is a powerful way to do that.

Continue reading ""Sell in May and Go Away" means working only two days a year" »

September 5, 2012

non-traded business development companies (BDCs): Good for the Broker, Bad for the Client

BDCs: Good for the Broker, Bad for the Client

In the wake of the implosion of many non-traded REITs, non-traded business development companies (BDCs) have emerged as a relatively new structure that is getting a lot of attention. But with high up-front fees and limited liquidity, some say they're not good for the client.

BDCs use a structure similar to non-traded REITs in that capital is raised in a continuous private offering, but BDCs are regulated under the 1940 Act that governs mutual funds. The big difference is that they're valued quarterly, while non-traded REITs are required to publish their valuations no later than 18 months after the conclusion of the offering.

May 11, 2012

ETFs over mutual funds

exchange-traded-funds (ETF) history lesson.

Exchange-Traded Funds

Ozgur Emre Ergungor

Cleveland Fed

May 7-9 was a great streak at Barry's BP.

May 7, 2012

VXX loses

Roll Yields'

That issue isn't disclosed until page 15 of the note's prospectus: "The existence of contango in the futures markets could result in negative 'roll yields', which could adversely affect the value of the index underlying your ETNs and, accordingly, decrease the payment you receive at maturity or upon redemption."

Kristin Friel, a spokeswoman for London-based Barclays, declined to comment.

The average ETN annual investor fee is 0.84 percent, according to Morningstar data. That doesn't include a lot of the tacked-on charges, Lee said. The UBS short VIX ETNs, for example, add about a 4 percent annual fee for "event-risk" hedging, leading to a total cost of 5.35 percent, he said.

Christiaan Brakman, a UBS spokesman, declined to comment.

April 23, 2012

$VXX goes down 80 percent of time

"Everyone knows" that US residential real estate is a bad investment, with the Case Shiller Home Price Index having dropped by about 32 per cent since its 2005 peak. At the end of last week, the iPath S&P 500 Vix Short Term Futures Exchange Traded Note had lost that much in one month. Not seven years. One month. Over the previous six months, the vehicle had lost more than 69 per cent of its value. The managers didn't do anything other than rigorously follow their charter, and their strategy has been fully disclosed, along with the trading history.

The reaction of some investors to this record is interesting: they have been doubling down. There has been a spurt of option buying on the ProShares Ultra Vix Short Term Futures Fund, which aims for twice the daily return for the Short Term Vix Futures Index.

Vix futures or options, you are not actually buying "volatility". Those products are based on the prices of forward start variance swaps. If you don't know what that means, don't buy Vix products.

January 18, 2012

Junk Munis ? Market Vectors High Yield Municipal Bond ETF (HYD)

Market Vectors High Yield Municipal Bond ETF (HYD)

This ETF was one of our picks for 2011, and delivered such an impressive return that we felt compelled to include it once again for the upcoming year. As the name suggests, HYD focuses on debt securities from municipal issuers that receive below investment grade ratings. Specifically, the underlying index consists of a 75% weight in below investment grade securities and a 25% allocation to Baa / BBB-rated bonds. Many of the securities found in HYD come from arrangements between municipalities and private corporations, which explains why about a quarter of the portfolio is dedicated to tobacco-related issuers [see High Yield ETFdb Portfolio].

Given the anxiety over the health of the muni bond market-especially high yield muni bonds with less-than-perfect credit ratings-it shouldn't be surprising that HYD can make a potentially attractive payout. For investors in the 25% tax bracket, the tax equivalent 30 day SEC yield is in the neighborhood of 7.7%; those in the top 35% bracket can get a return equivalent closer to 8.8%.

January 10, 2012

Inverse volatility: XIV, not VIX

VelocityShares Inverse VIX ETN (XIV)

This ETN offers daily inverse exposure to an index comprised of investments in short-term VIX futures contracts-a strategy that has struggled mightily in 2011 thanks to heightened volatility and backwardated markets. Though XIV has lost more than 40% of its value in 2011, there is reason to be optimistic that at least the beginning of 2012 will be more favorable. The VIX, a measure of expected equity market volatility, has declined considerably in recent weeks as optimism over the global economy has returned. And more importantly for XIV, contango in VIX futures markets has also returned; the futures curve now has a steep upward slope, a condition that can give a nice boost to the strategy employed by XIV [see also Low Volatility ETFs Attracting Big Inflows].

Given that XIV utilizes a futures-based strategy to deliver inverse exposure, this ETN probably isn't appropriate for risk-averse investors who aren't willing or able to regularly monitor their positions. But for those who grasp the complexities associated with XIV, the current environment might just be perfect for this ETN. XIV might not be a good ETN to own throughout 2012, but it certainly seems to be positioned nicely for a strong start to the year.

January 7, 2012

ETF for Greek recovery ?

Global X FTSE Greece 20 ETF (GREK)

This ETF pick is purely a contrarian play-and an admittedly risky one at that. GREK offers a way to invest in the Greek stock market, which has seen close to 90% of its value erased over the last few years as the country has been pushed to the brink of fiscal collapse. While the recent past has been catastrophic, there is opportunity to capture some material gains if Europe is able to pull Greece back from the brink. The developments in the ongoing debt saga have actually been quite positive in recent weeks, as private investors have agreed to haircuts on bond holdings and efforts to implement badly-needed cuts to government spending have gained some momentum [see also Three Long/Short Ideas For Euro Drama].

GREK is perhaps the best opportunity to live out the old Buffett mantra of "being greedy when others are fearful." At a time when most investors won't touch Greece with a ten foot pole, GREK offers a way to tap into a market that could be bottoming out. GREK is essentially a bet that Greece doesn't meet complete collapse in the new year, and can certainly be expected to exhibit a fair amount of volatility. For the risk tolerant crowd, we believe this ETF has some opportunity to surprise in 2012.

January 4, 2012

EGShares Small Cap India ETF (SCIN)

EGShares Small Cap India ETF (SCIN)

This pick is more of an opportunistic buy of an asset class that has potential to deliver huge returns over the long run. The Indian economy is expected to eventually become the second-largest in the world, posting growth rates over the next several decades that surpass even China. Small cap companies that rely on growth in local consumption should be ideally positioned to profit from a swelling middle class, ongoing urbanization, and general increases in wealth and improvements in quality of life [see Evaluating India ETFs: Three Important Factors To Consider].

SCIN's struggles in 2011 allow investors to tap into this investment theme at a big discount; this fund has lost more than 40% of its value in 2011 as a result of inflation-related concerns, corruption, and general risk aversion. India is frustrating to many investors: a massive economy with tremendous untapped economic potential that has repeatedly stumbled in its attempt to increase its presence on the global stage. SCIN could definitely have more short-term volatility ahead, but this fund could deliver some impressive returns to those willing and able to hold on for the long haul.

March 24, 2011

Emerging markets individual countries ETFs and exchange-traded mutual funds

Funds and ETFs

The best way to play individual countries is through exchange-traded mutual funds. You can track Russia via the Market Vectors Russia exchange-traded fund, Mexico via the iShares MSCI Mexico Index ETF and Taiwan via the iShares MSCI Taiwan Index ETF, among others.

Placing individual country bets isn't for the timid, however. Emerging markets are notoriously volatile, and single-country ETFs are susceptible to big swings. "These ETFs can have enormous years on the upside and enormous years on the downside," says Howard Sontag, chief executive of Sontag Advisory LLC in New York.

With correlations breaking down, the safest way to play emerging markets is to invest in a broad range of nations. You might assume that diversified index funds or ETFs would be a good vehicle. But those tend to be dominated by the biggest companies in the biggest markets--China and India among them.

"You can't just invest in the aggregate index," says Nuno Fernandes, a professor of finance at the International Institute for Management Development in Lausanne, Switzerland. "You have to do a better job of choosing where to invest."

An actively managed mutual fund might be a better alternative, because the manager, in theory, has the expertise to make the difficult strategy calls that most individual investors can't. To find the most experienced, scour fund websites for information about managers, and look for tenures of five years or longer or other emerging-markets experience.

The top performer during the past three years has been the Aberdeen Emerging Markets Institutional Fund, which gained 11% annually, according to investment-research firm Morningstar Inc. As of the end of January, it had 17% of its portfolio in Brazil, about one percentage point more than the MSCI Emerging Market Index--and just 5% in South Korea, versus 7% for the index.

The best performer on a five-year basis is the Wells Fargo Advantage Emerging Markets Fund, returning 13% annually. As of the end of February, Korea made up just 10% of the portfolio versus 15% for its benchmark, while Mexico accounted for 5.6%, more than the benchmark's 4.5%. The fund focuses on companies more than countries, says portfolio manager Jerry Zhang.

The menu of actively managed portfolios is growing. Firms have rolled out 23 new diversified emerging-market funds during the past 12 months, according to Morningstar, compared with six in the year-earlier period. There are 135 actively-managed emerging-market funds overall, according to Morningstar.

A caveat: Most actively managed funds lag the index over time. And for some of the firms rolling out new funds, this will be their first emerging-markets product. Among them: Marsico Funds, Baron Funds and Fred Alger Management Inc.'s Alger Funds.

Continue reading "Emerging markets individual countries ETFs and exchange-traded mutual funds" »

December 16, 2008

Greeks of leveraged ETFs

Ultra ETFs deliver a 2 delta. There is a negligible amount of gamma, theta, and vega, a small amount of rho, and some exposure to dividend risk and borrowing costs.

-- ET comment on the option greeks of ETFs.

December 11, 2008

3x ETF: bulls and bears

Bespoke notes the launch and raid growth of 3x ETF.

Many have argued that these ETFs are contributing to the volatility of the market due to their leverage. While the huge swings in these things are tempting, the losses can pile up fast with just one bad trade. For the last several months, we have learned how excess leverage has threatened the entire system. After all of this, what kind of message does it send to start creating securities that allow anyone, regardless of their investment experience, to leverage up three times with the simple click of a mouse? Before the introduction of these ETFs, the only way for an individual to increase leverage was through margin borrowing or option trading. Both of these require the brokerage to clearly highlight the potential risks and the investor to acknowledge them. Yet with these ETFs, some investors are potentially leveraging up without knowing the risks involved.

Examples:

Financial: FAS bull, FAZ bear

Russell 1000: BGU bull, BGZ bear

First there was 2x, now 3x, do I hear a 5x.

September 2, 2008

August 16, 2008

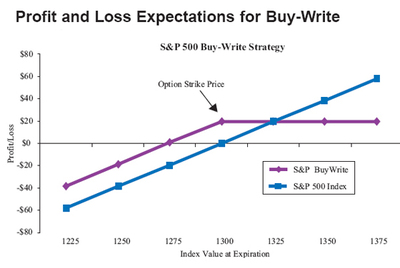

Buy-Write covered calls: BEP and BWV

There are many funds today offering some version of covered call strategy (BuyWrite strategy). We have been asked "What do they do?" and "Are they a good addition to a diversified and allocated portfolio?"

In September 2004 the Ibbotson Associates consulting found higher returns and much lower volatility for a the BuyWrite index versus the S&P 500 alone.

-- qvmgroup

August 15, 2008

Index Exchange-Traded Funds (ETFs), etfconnect

ETF Connect reports on exchange traded funds.

Index Exchange-Traded Funds (ETFs) and Closed-End ETFs (CEFs) feature

intra-day trading and stock exchange listing. They rapidly are changing

the way many financial advisors and investors manage their portfolios.

Index ETFs, including SPDRs, Diamonds and HOLDRS.

Closed-End ETFs, including municipal bond and country funds.

August 11, 2008

Index Universe

indexuniverse covers US-listed ETFs and index funds.

Example:

assests are up:

* Assets in US REIT ETFs have increased 15.4%.

* Assets in commodity ETFs saw assets grow by 34%.

* Assets in TIPS, or Treasury inflation-protected securities ETFs increased by 39%.

The new SPDR DB Inflation-Protected Securities ETF (WIP) was launched in March 2008 as the first and only ETF to offer access to international inflation-protected bonds. WIP had gathered $183 million in assets as of June 30, 2008.

July 30, 2008

ETF Express

etfexpress.com surveys the plethora of ETF investment options.

News of who's who and where, for industry insiders; produced by Hedgemedia.

July 24, 2006

Foreign ETFs of Bill Gross

July 23, 2006

Varying observation window portfolio stress test

Portfolio stress test by varying the observation window, at Seeking Alpha.

The difference in projected portfolio performance as a reflection

of the changing dynamics of foreign markets. As globalization

increases, some other economies are more coupled to the U.S.

economy and—perhaps more important—are perceived as

being more coupled to the U.S. economy. Further, as more

domestic investors put an increasingly heavy allocation into

foreign stocks, we will naturally see more coupling in returns

and there will be a decreased level of diversification effects

available from investing in many foreign economies.

July 20, 2006

ETF: Exchange-Traded Funds

ETF Trends and ETF centre at Seeking Alpha track Exchange-Traded Funds.

January 25, 2005

ETF

ETFs are shares of a basket of stocks bought and sold as a single

investment. Investment companies create these stocks by buying the

underlying stocks and issuing ETF shares. Unlike mutual funds whose

price is set once per day, ETFs trade on stock exchanges at

constantly changing market prices. This prevents market timers

getting preferential prices like the recent mutual fund scandals.

Very large investors can issue new shares or redeem their shares for

the underlying stocks. This keeps the ETF price close in price to the

underlying shares. ETFs do not trade at sizable discounts or

surpluses to the underlying stocks like closed end mutual funds. If

the ETFs begin to trade with any significant discount or surplus,

large investors will issue new shares or redeem their shares to

eliminate the discount or surplus.

December 30, 2004

ETF exchange traded funds

Probably the biggest eye-catcher is iShares FTSE/Xinhua China 25

Index Fund (FXI) — the first ETF investing solely in China

available to U.S. investors. Launched earlier this month,

the ETF tracks the 25 largest and most liquid Chinese stocks.

Of course, there's increasing talk of China's red-hot economy

cooling, but few expect the growth spigot to be shut entirely.

The China 25 Index Fund's expense ratio of 0.74% is higher

than that of most ETFs, but it's substantially lower than the

average China-region mutual fund's expense ratio of 2.37%,

according to Lipper. ETFs, by nature, carry lower expense ratios

than their mutual-fund counterparts. [1]

Standard and Poors index tracker.